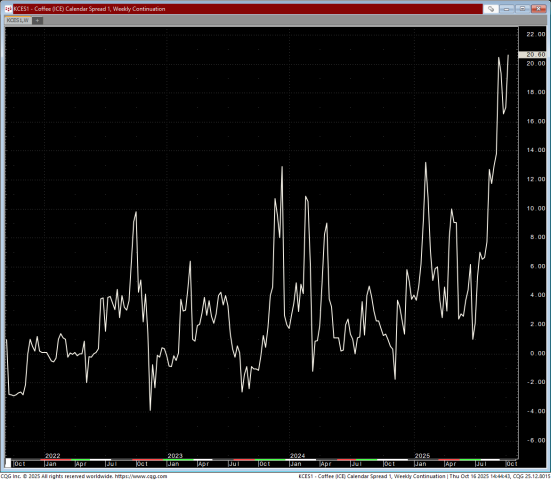

The coffee market has entered rare territory. For the past two years, the C-market has remained in backwardation, an inversion where nearby contracts trade at a premium to future months. That inversion has deepened sharply in recent weeks. The spread between December 2025 and March 2026 is now more than 20 cents per pound, and the December–July difference is close to 50 cents.

Below is the current ICE (Intercontinental Exchange) Coffee (KC) calendar spread, showing how the near-term premium has surged:

ICE Coffee (KC) Calendar Spread — Weekly Continuation. Source: CQG Inc., October 2025

- Near-Term Prices Surge on Brazil and Colombia Tensions

The week began with further gains. On Monday, the December contract in New York climbed 990 points, or 2.5%, to 407.35¢ per pound. In London, the January Robusta contract rose $38 per metric ton, or 0.85%, to $4,516 per ton. These movements are being driven by two overlapping issues: weather stress in Brazil and worsening diplomatic tensions between the United States and Colombia.

The U.S. president recently issued sharp public criticism of Colombian president Gustavo Petro and raised the possibility of imposing tariffs on Colombian coffee. The threat has unsettled the U.S. market, which relies heavily on Colombia as a key supplier. In 2024, Brazil accounted for 35% of U.S. coffee imports, while Colombia supplied 20%. Any trade restriction on Colombia would tighten the U.S. supply chain even further and add upward pressure to New York prices.

- Spot Inventories Remain Critically Low

ICE-monitored arabica inventories have fallen to around 495,000 bags, the lowest in over a year. Robusta inventories hover near 6,200 lots. These are historically tight levels that magnify the market’s sensitivity to any new supply risk. When certified stocks fall this far, the value of physical coffee increases. Traders refer to this as the “convenience yield,” but in practical terms it means roasters must pay a premium for immediate delivery.

- Tariffs and Policy Uncertainty Distort Trade Flows

The existing 50% tariff on Brazilian green coffee imports continues to disrupt U.S. trade flows. American importers have canceled or deferred contracts, forcing exporters in Brazil to redirect shipments to other destinations. The result is a structural shortage in the U.S., even as global output remains adequate.

Now, the potential for Colombian tariffs adds a second front of risk. Together, these developments threaten to squeeze supply from both major U.S. origins simultaneously. Until policy stabilizes or tariffs are lifted, it’s difficult to envision a meaningful rebuild of U.S. inventories.

- A Market That Can’t Normalize

To restore balance, two conditions must occur:

- Consuming-country inventories must rebuild, particularly in the U.S., back toward the 3–4 million bag level on ICE.

- Tariff barriers must ease, both on Brazilian and potentially Colombian coffee.

Without those adjustments, backwardation will persist. The futures curve is sending a clear signal: near-term coffee is scarce, and buyers are paying up for what little supply exists.

- What Roasters Should Take from This

The inversion affects procurement timing, hedging, and working capital.

- Near-term supply will remain expensive.

- Deferred futures may offer better nominal pricing but carry storage, financing, and basis risk.

- Traditional hedge models won’t behave as expected in this environment.

This is a market that rewards planning and informed partnerships.

- Work With the Royal Trading Team

The Royal trading desk monitors these shifts daily: ICE inventories, origin differentials, tariff policy, weather, and logistics. Our job is to translate that complexity into an actionable strategy for our customers.

We can help you:

- Secure forward coverage that fits your production schedule.

- Diversify sourcing to mitigate tariff exposure.

- Evaluate how market spreads affect your landed cost and timing.

If you’d like to review your position or discuss upcoming shipment opportunities, contact trading@royalcoffee.com or reach out to your Royal representative.

Closing Thoughts

The combination of low certified stocks, tariff-driven trade friction, and geopolitical uncertainty in Brazil and Colombia has created one of the tightest near-term markets in memory. Until inventories rebuild or policy risk subsides, backwardation and high nearby premiums will continue to define the C-market.

Royal Coffee remains committed to helping roasters navigate this environment with clear data, disciplined strategy, and dependable supply partnerships.

Latest Articles by Max Nicholas-Fulmer

What Does the Supreme Court Tariff Hearing Mean for Coffee?

The Supreme Court’s recent hearing on the IEEPA tariffs signals skepticism about presidential trade powers but no quick relief for importers. Refunds appear off the table, and tariff risk, especially...

Tariff Updates: What’s Changing and What to Watch

Editor’s Note August 20th: Brazil: A 50% tariff on green coffee takes effect August 6, with no exemption granted. The increase is tied to recent political tensions and was confirmed by Commerce Secretary...

Understanding the Impact of New Tariffs on Coffee Imports

Editor’s Note: The White House is clarifying that Trump’s announcement of a 90-day tariff “pause” means that the “tariff level will be brought down to a universal 10% tariff” during...