Time Keeps on Slipping…into the Future

The C Market is finally starting to come under some selling pressure, but there is still a large area of support at the 215.00 to 220.00 area. It would be premature to assume the market can or should break much lower than that in the near term. Remember: we are still in both Brazilian frost and Atlantic hurricane seasons. It has been a quiet year for news on both fronts, but things can change in hurry. And, right after frost season concludes at end of August, the annual rainfall watch in Brazil begins, as coffee trees need regular rains to set the flowering for the next crop.

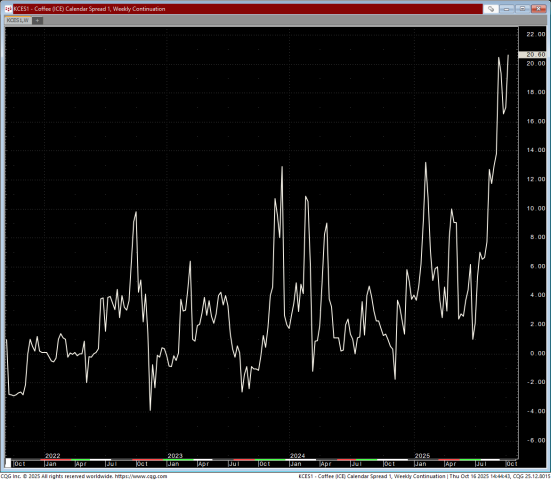

Backwardation (the relatively unusual condition wherein the SPOT NYC month is higher than the further out months) is still holding, but the spread is getting tighter, indicating improved nearby coffee flow. CECAFE, the Brazilian coffee authority, is reporting preliminary data showing 1 million bags of Conilon Robusta being shipped in the month of July. This would be a record if confirmed, and exporters are saying it could have been even higher, if not for shipping delays, which are back worldwide after an 18-to-24 month hiatus. As alluded to in our last update on Ethiopia, Suez Canal transits are down to less than 10% of where they were just 9 months ago. The waterway at the end of 2023 accounted for 200,000 20-foot container load transits per day, or 30% of global traffic. Vessels enroute to Europe and the Americas are now rerouting around the Cape of Good Hope, adding weeks to the journey and accounting for a substantial increase in fuel surcharges, not to mention overall costs. The longer the global containership fleet has to be at sea, the less spare capacity there is. Speaking of costs, the price to ship on the Shanghai to US West Coast routing, the busiest containership lane in the world (and how virtually all East African and Indo-Pacific coffees eventually make it here) is now back to 90% of the high we saw in 2021-2022 during the pandemic shopping spree.

What does it all mean?

SPOT coffee is once again king, with the very important corollary that it has never been more important to book at least some coffee in advance. The cost of financing a coffee position is still quite high, leading many importers (*ahem*) to scale back on SPOT inventory this year. As we come into South American and Indonesian arrivals season, some of this will eventually ease, but the reality is that you cannot expect to cover all your needs from SPOT purchases all the time, for the foreseeable future.

Make a plan with your Royal Coffee trader to book your must-have’s, and as always, try to be flexible in accommodating recipe changes. Colombia and Peru are excellent Central substitutes that will be fresher, brighter and, in many cases, somewhat lower priced. If you need a refresh on coffee seasonality, check out our Roasters Guide to Coffee Seasons blog post.

Latest Articles by Max Nicholas-Fulmer

What Does the Supreme Court Tariff Hearing Mean for Coffee?

The Supreme Court’s recent hearing on the IEEPA tariffs signals skepticism about presidential trade powers but no quick relief for importers. Refunds appear off the table, and tariff risk, especially...

Coffee Market Update: Backwardation and What It Means for Roasters

The global coffee market has entered uncharted territory. Tight inventories, Brazil tariffs, and U.S.–Colombia trade tensions are pushing C-market prices higher and sustaining extreme backwardation. Learn what it means for...

Tariff Updates: What’s Changing and What to Watch

Editor’s Note August 20th: Brazil: A 50% tariff on green coffee takes effect August 6, with no exemption granted. The increase is tied to recent political tensions and was confirmed by Commerce Secretary...

Hey, Max. Helpful and insightful analysis for roasters. Love the title! Thanks for all you do.